This is Xavier Giné at the World Bank

Part of the take-up problem, especially in the case of savings, is that some of these products are pretty crappy. If we see no demand for these products, maybe that’s a good thing actually. If you put money into one of these accounts, check the balance a few times, make a few withdrawals, half or all the money has been eaten up by fees. So the characteristics of the product are very important.

That’s from Tim Ogden’s Experimental Conversations: Perspectives on Randomized Trials in Development Economics.

Beyond savings products, this is important because there is a temptation to lump interventions together (How effective are home-based child care visits? How effective is teacher training?) when in fact there is massive diversity in the particulars of the interventions. Sara Nadel and Lant Pritchett have referred to this as “high dimensional design space,” and Popova et al. document it in the case of teacher training interventions.

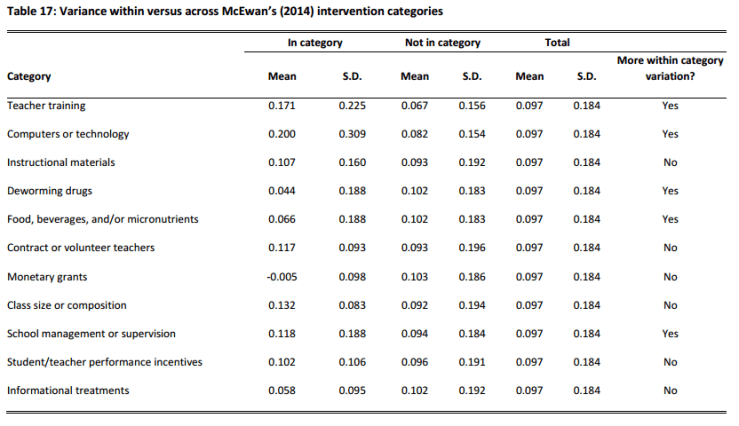

There is no reason to believe — ex ante — that all interventions in the same “category” will have the same effect. Indeed, in work Anna Popova and I did analyzing randomized controlled trials of education interventions, we found that in many cases, the variation in impact within categories exceeded the variation across categories, per the table below.

So, as Giné says, “the characteristics of the product are very important.”